Summary

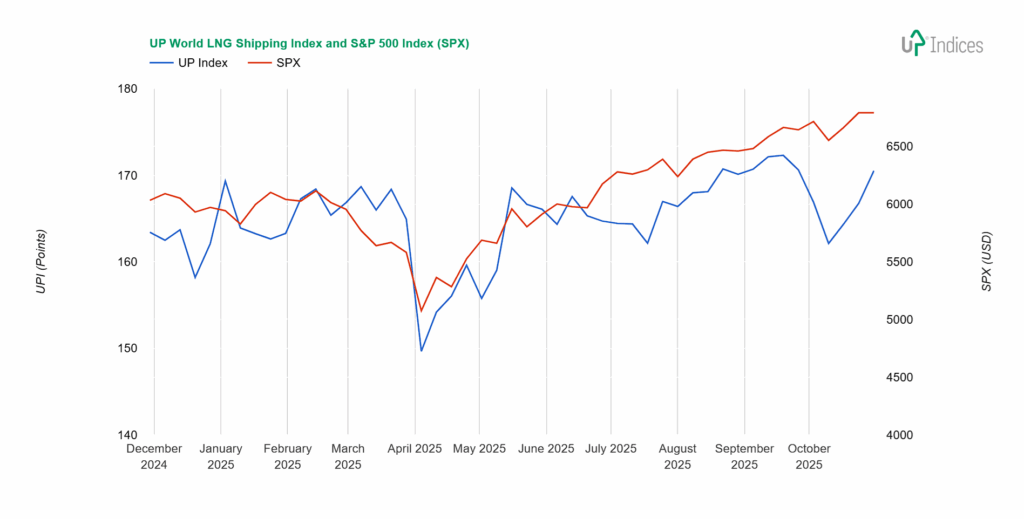

This rebound underscores renewed investor confidence in LNG shipping and confirms the strength of support at 160 points. Strong quarterly results, rising spot and long-term charter rates, and the gradual replacement of older steam vessels all contributed to the positive sentiment. Most UPI constituents advanced, led by COSCO Energy Transport and Golar LNG, while only a few—most notably New Fortress Energy—declined. With firm technical support and increasing volatility, the outlook remains optimistic in the longer term.

UPI & SPX

The UP World LNG Shipping Index, which tracks listed LNG shipping companies, gained 3.78 points (2.27%), closing at 170.53 points, while the S&P 500 index gained 0.71%. The chart below illustrates the performance of both indices with weekly data.

Broader View

UPI is once again above the 170-point mark. This is good news for two reasons. Firstly, investor interest in LNG shipping companies is returning, and secondly, this growth confirms the strength and importance of support at 160 points.

Of course, the growth of the UPI is beginning to reflect 1) the published quarterly results for the third half of the year, 2) positive sentiment in the sector, 3) rising spot rates, and 4) confirmation of long-term rates.

Nakilat, Capital Clean Energy Carriers, BP, and Shell published their quarterly results, Golar LNG added a report on the conclusion of an Argentine contract, and Spark Commodities reported a sharp week-on-week increase in spot rates of $26,000 to $61,000 per day.

In addition to the figures, the quarterly results also provided information on the demand for LNG tankers. According to CCEC, the withdrawal of first-generation LNG tankers from the market continues: “Since the second quarter, there has been a sustained rise in steam and tri-fuel vessels stan-ding idle, around 16% to 18% of steam vessels, which is approximately 35 ships sitting idle, which means that nearly 1/5 of all steam vessels stand without long-term or spot employment,” says Nikolaos Tripodakis, COO of CCEC, adding: “According to brokers, 86 steam LNG carriers are due to come off long-term time charter contracts between now and 2030, which reflects approximately 45% of the entire steam fleet.” Long-term contracts remain above $80,000 per day, significantly higher than spot rates, as confirmed by the development of our UPI TCE indicator, which currently stands at around $70,000 per day. UPI TCE includes existing fleet contracts from the UP World LNG Shipping Index. In fact, we also noted recently in our weekly reports that spot rates are no longer a scare tactic for investors. As Oystein Kalleklev, then CEO of Flex LNG, pointed out at the turn of the year, this year will be marked by the rejuvenation of the global LNG fleet. The completion of new LNG terminals is also playing a positive role.

The ratio of rising to falling companies was 13:5, with one company remaining unchanged throughout the week. The median movement was +1.84%, and trading volume was well above average.

Constituents

We will begin our summary of companies with Capital Clean Energy Carriers (NYQ: CCEC), which announced the conclusion of a ten-year (7+1+1+1) contract for its LNG newbuild, scheduled to enter service in the first quarter of 2027. The contract is worth around $90,000 per day. The contract is therefore missing for three tankers under construction. The company’s shares closed the week with a 3.7% loss and stopped at support, meaning the price was lower during the week. Overall, CCEC has been moving sideways this year.

COSCO Energy Transport (SS: 600026) experienced the most significant growth, at 10%. It continues the growth trend that began in the summer.

Golar LNG (NYQ: GLNG) added 7.7% after announcing the aforementioned Argentine contract. Despite this increase, the stock is still moving sideways.

Growth of more than 3% was also recorded by Tsakos Energy Navigation (NYSE: TEN, +4.64%), Korea Line Corporation (KRX: 005880, +4.45%) and Flex LNG (NYSE: FLNG, +3.96%). TEN broke through resistance and continues to grow, albeit at a lower volume. KLC rose to resistance and could attempt a breakout this week. FLNG also reached one of its resistance levels. However, the main one awaits it at $27.

Four companies grew by double-digit percentages: Exmar (BSE: EXM, +2.5%), NYK Line (TSE: 9101, +2.34%), “K” Line (TSE: 9107, +2.26%), and Mitsui O.S.K. Lines (TSE: 9104, +2.03%). We can also add Dynagas LNG Partners (NYSE: DLNG), which has a growth rate of 1.98%.

Exmar remains close to being delisted, as reflected in its low trading volume. The Japanese trio has been moving forward as one for the third consecutive week. However, while NYK Line and “K” Line have rebounded from support and are rising in a sideways range, MOL is only slowly approaching the broken support, which has now become resistance. DLNG has been steadily moving at support since spring.

MISC (KLSE: 3816) is worth mentioning, as it grew by only 0.5% but averted a significant decline and remained at its resistance level.

New Fortress Energy (NYQ: NFE) again recorded the most significant decline, falling 25% and returning to its lowest values. If we were optimistic, we would say it has returned to its support level.

After CCEC, which we mentioned at the beginning, ADNOC L&S (ADX: ADNOCLS) had the third-largest weekly loss, falling 2.71% and forming a resting island above the August-December 2024 prices.

The remaining two declining companies are Excelerate Energy (NYQ: EE) and Nakilat (QSE: QGTS). EE lost 1.86% and Nakilat 1.21%. EE had a similar week to the previous one, as it again averted a more profound decline. Given the candlestick formation on the chart, one could infer a continuing upward trend. Nakilat is creating its support, where it has been hovering for the third week. However, from a more distant perspective, this is an extension of a limit that began at the start of this year, so the renewal of this support is no longer a mystery. According to its position on the candlestick chart, the company’s performance is growing, although its annual stock performance will not be excellent at this time.

Crystal Ball

The late-summer rise was rejected, and UPI returned to its previous range, where it now trades. This area provides firm support. In the short term, we estimate a rise in volatility of UPI´s constituents.

Our outlook remains steadfastly positive in the long term. The burgeoning demand for LNG, bolstered by situational or management-driven actions and the potential for new long-term contracts, paints a promising picture. Investors should watch policy developments, market competition, and upcoming corporate earnings for further direction.

About UPI

Established in 2020, the UP World LNG Shipping Index is a rules-based stock index family designed to measure the performance of publicly traded companies worldwide involved in the maritime transportation of liquefied natural gas (LNG). This unique index covers 21 companies and partnerships worldwide, representing over 65% of the world’s LNG carrier fleet in 2020. The UP Index provides premium services, offering freemium and trial access to charts. With Freemium, users can access the basic UPI vs. S&P 500 chart after completing an email registration. The trial includes full access for fourteen days.

Final Note

This report primarily relies on technical analysis using weekly data.