Summary

The UP World LNG Shipping Index gained 6.67 points (2.97%) last week, closing at 231.04 points — surpassing the 230-point mark for the first time in its history — while the S&P 500 gained 3.36%, posting its first weekly gain in six weeks. The UPI has now recorded a 36% increase over the first three months of 2026, demonstrating resilience through two brief corrections, both of which were followed by stronger advances. Ten companies gained, nine declined, and one was unchanged; the median change was 0%. Trading volume remains above average, though gradually normalising. The initial shock to the LNG market is giving way to a lull, with spot tanker rates continuing to ease — Atlantic rates at $92,000/day and Pacific at $86,000/day according to Spark Commodities — driven by reduced demand and the first LNG production milestone at the Golden Pass terminal in Texas.

Tsakos Energy Navigation led the gainers with a +5.37% gain, returning to uncharted territory after its recent correction. COSCO Shipping Energy Transportation added 4.9%, while NYK Line rose 4.5% and ADNOC Logistics & Services gained 4.2%, rebounding from wartime support levels. The most notable declines were posted by Capital Clean Energy Carriers (–8%), New Fortress Energy (–6.56%), and Chevron (–5.77%). Golar LNG added 0.47%, supported by its ongoing strategic review with Goldman Sachs. The short-term outlook remains volatile; long-term fundamentals stay positive.

UPI & SPX

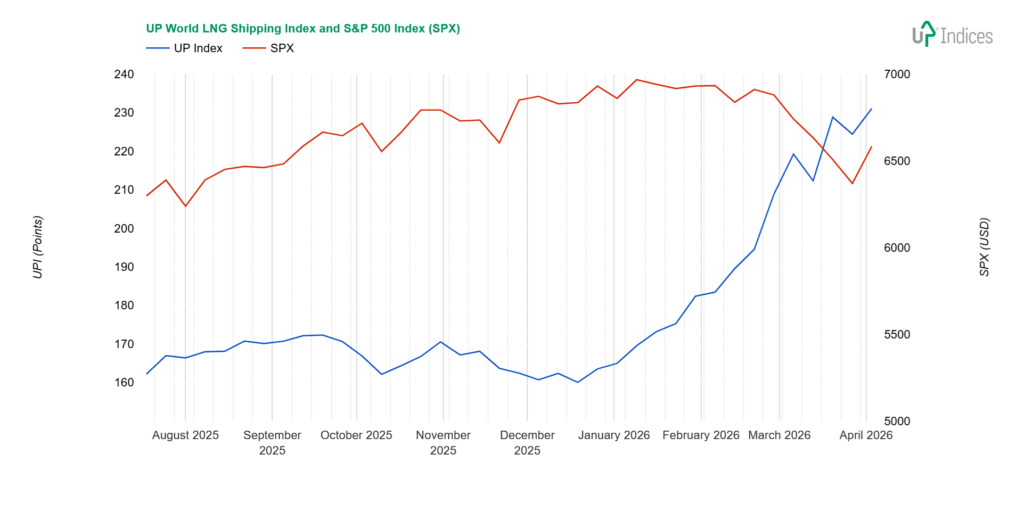

The UP World LNG Shipping Index, which tracks 20 listed LNG shipping companies, gained 6.67 points (2.97%), closing at 231.04 points, while the S&P 500 index gained 3.36%. The chart below illustrates the performance of both indices with weekly data.

Broader View

For the first time in its history, the UPI has surpassed 230 points. This came after a one-week correction. The UPI is thus demonstrating its strength, as it has recorded two declines so far this year, both of which were followed by stronger growth. It is no wonder, then, that the UPI has posted a 36% increase over the first three months of this year!

10 companies drove last week’s growth, while 9 saw their shares fall and 1 remained unchanged. The median change was also 0%.

Trading volume remains above average, although the average volume has been rising sharply following the attack on Iran.

Although the geopolitical situation has not changed much, the initial shock to the LNG market is giving way to a lull, even as prices remain much higher than before. According to Reuters’ weekly summary, spot LNG rates for both Asia and Europe have weakened, driven by reduced demand and the first LNG production at the U.S.-Qatar Golden Pass terminal.

Spot rates for LNG tankers also continue to decline slightly but remain at interesting levels. According to Spark Commodities, they stood at $92,000 for the Atlantic route and $86,000 for the Pacific route.

Constituents

No movement was in the double digits last week. Since the UPI rose, we’ll start with the stocks that gained.

Tsakos Energy Navigation (NYSE: TEN) posted the largest gain. It rose 5.37%, and the price thus returned to uncharted territory following the correction.

COSCO Shipping Energy Transportation (SS: 600026) recorded the second-largest gain, rising 4.9%. Its share price has been trading sideways in the 22–26 yuan range for the fifth consecutive week.

NYK Line (TSE: 9101) was the only Japanese company to see significant growth, posting a 4.5% gain. This offset the decline from the week before last, which, as we noted, had a positive candlestick pattern on the candlestick chart. As a result, the price closed a few tenths higher than two weeks ago.

In fourth place is ADNOC Logistics & Services (ADX: ADNOCLS), which rose 4.2% as the price rebounded from its wartime support level around five dirhams. This, too, suggests growing optimism or adaptation to the situation.

Only smaller gains remain. Korea Line Corporation (KRX: 005880) gained 1.5%, but, as last week, the price saw significant upward and downward movements and is now moving sideways.

Shell (NYSE: SHEL) rose by one per cent, but the small red body and long wicks and shadows point to an ongoing tug-of-war over the next direction.

BP (NYSE: BP) and FLEX LNG (NYSE: FLNG) both posted identical gains of 0.94%. While BP had a candle similar to Shell’s—a small red body with a longer wick and shadow—FLEX reversed its decline, and the price returned to the resistance level at which it opened earlier in the week.

Nakilat (QSE: QGTS) saw significant movement during the week, but the result was a slight 0.9% gain.

The weekly candle for Golar LNG (NASDAQ: GLNG) also had a small body, as it too fended off an attempt to decline. The result is a weekly gain of 0.47% and, more importantly, a generally positive candle, which may signal continued growth.

On the downside, there were three significant losses: Capital Clean Energy Carriers (NYSE: CCEC) lost 8% and fell just below two support levels. The area around $18 offers stabilisation.

The second significant percentage decline was seen in New Fortress Energy (NASDAQ: NFE). It fell by 6.56%, which, in its case—where we’ve been accustomed to double-digit movements—is actually a smaller move. However, it shows that the approved restructuring is being viewed negatively by current shareholders.

Third on the list is Chevron (NYSE: CVX), which lost 5.77% and thus did not follow the trend of its two oil-and-gas peers. On the other hand, it is worth noting that this decline, having started higher than the previous closing price, is smaller than the gain from the week before last.

Three companies lost around two per cent: “K” Line (TSE: 9107) fell by 2.62%, Dynagas LNG Partners (NYSE: DLNG) lost 2.58%, and Exmar (EBR: EXM) dropped by 2.5%. “K” Line corrected with a green weekly candle, as its opening price was at the level of the previous minor support. Although the gap was closed during the week, the closing price was lower. The green candle thus indicates a weekly decline.

Dynagas LNG Partners has not yet decided to attempt a breakout above the $4.40 resistance level, but it also does not want to move lower. Exmar continues to trade sideways.

Awilco LNG (OSE: ALNG) continues to trade sideways, but there were only attempts at an uptrend during the week. As a result, the price fell by 0.15%.

Crystal Ball

The outlook remains volatile and unpredictable. Companies with spot LNG tankers are maintaining positive momentum, benefiting from high spot rates and increased distances.

The long-term outlook remains positive. The scrapping of steam vessels and the addition of new liquefaction capacity are pushing the sector higher.

About UPI

Established in 2020, the UP World LNG Shipping Index is a rules-based family of stock indices designed to measure the performance of publicly traded companies worldwide engaged in the maritime transportation of liquefied natural gas (LNG). This unique index comprises 20 companies and partnerships worldwide, representing more than 65% of the global LNG carrier fleet in 2020. The UP Index provides premium services, offering freemium and trial access to charts. With the Freemium plan, users can access the basic UPI vs S&P 500 chart after completing email registration. The trial includes full access for fourteen days.

Final Note

This report primarily relies on technical analysis using weekly data. The summary section is AI-generated.