Summary

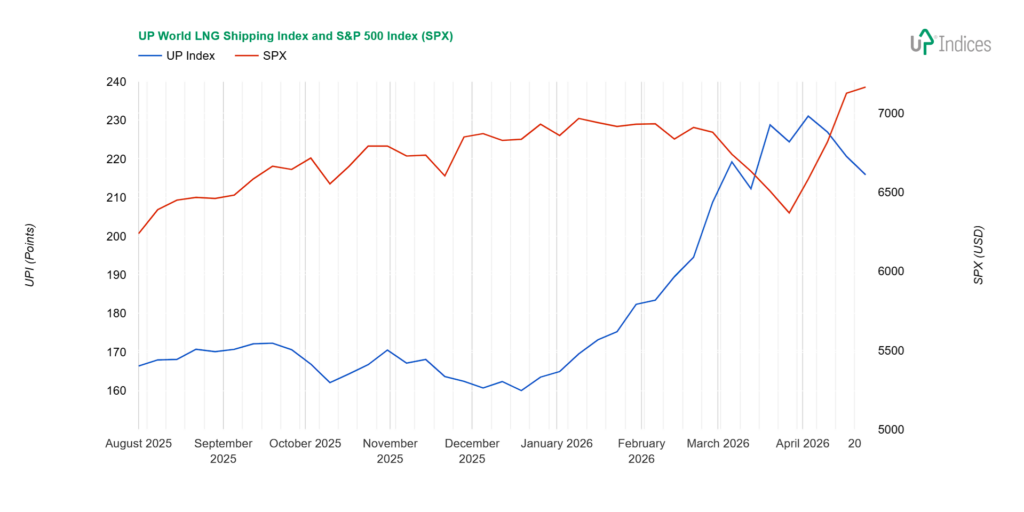

The UP World LNG Shipping Index lost 4.75 points (2.15%) last week, closing at 215.86 points, while the S&P 500 gained 0.55%. The UPI has now declined for three consecutive weeks, though this does not signal the start of a bear market — the index is consolidating after its exceptional first-quarter run. Eight companies gained, eleven declined, and the median change was -0.33%. Trading volume fell significantly, returning to levels seen at the start of the year.

The Strait of Hormuz remains closed, with LNG continuing to reach customers via longer alternative routes. Argentina, Pakistan, and Bangladesh issued new spot tenders last week. Spot rates were virtually unchanged: $103,000/day for the Atlantic route and $71,000/day for the Pacific, according to Spark Commodities. Asian LNG demand grew last week, and arbitrage conditions favour Asia over Europe for the coming month. A potential return of China to the spot market could further boost demand and increase pressure to resolve the US–Iran conflict. Awilco LNG led the gainers with a +5% gain, followed by Exmar (+3.94%) and BP (+3.72%). New Fortress Energy suffered the largest loss at -7.36%, while K Line fell 4.34%, and five companies each declined around 3%. The long-term outlook remains positive, supported by vessel scrapping, new liquefaction capacity, and the structural shift toward longer shipping routes.

UPI & SPX

The UP World LNG Shipping Index, which tracks 20 listed LNG shipping companies, lost 4.75 points (2.15%), closing at 215.86 points, while the S&P 500 index gained 0.55%. The chart below illustrates the performance of both indices with weekly data.

Broader View

The UPI has been declining for the third week in a row. Nevertheless, it cannot be said that a bear market is beginning. Like many companies, the UPI is tired and seems to be taking a breather, albeit somewhat resignedly.

Eleven companies weakened and eight strengthened. The median change was -0.33%, and the volume of shares traded fell significantly, returning to levels seen at the beginning of the year.

The geopolitical situation remains uncertain and unstable. The Strait of Hormuz remains closed, and LNG is flowing to its customers via other (longer) routes. Over the past week, reports emerged of new tenders for spot deliveries, e.g., for Argentina, Pakistan, or Bangladesh.

Spot rates for LNG tankers remained virtually unchanged. According to Spark Commodities, the rate for the Atlantic route is $103,000, and for the Pacific route, $71,000. The Atlantic route is also used to transport U.S. LNG to Asia.

Asian demand for LNG grew last week, according to Reuters. Citing Spark Commodities, it further noted that arbitrage prices for the coming month are higher in Asia than in Europe. Demand could be further boosted by China’s return to the spot market, which would also increase pressure to resolve the U.S.-Iran conflict or at least reopen the Strait of Hormuz.

U.S. LNG producers continue in their expansion: Cheniere is close to launching the sixth train at Corpus Christi.

Constituents

New Fortress Energy (NASDAQ: NFE) recorded the biggest loss, falling 7.36%. Despite this, it is currently trading sideways near historic lows.

“K” Line (TSE: 9107) suffered the second-largest loss, down 4.34%. In its case, hesitation over the next move turned into a test of the support zone, which halted the decline and triggered a slight rebound. “K” Line is in a similar situation to the entire UPI—after rising at the turn of the year, it ran out of steam, but it is not ready to give up yet and hopes that mild declines will lead to new growth. That may happen, but a rapid decline—a sobering-up from the growth—could also occur.

Five companies saw a 3% decline. And if we were to round up, there would be six: NYK Line, Capital Clean Energy Carriers, Excelerate Energy, COSCO Shipping Energy Transportation, and ADNOC Logistics & Services. The sixth is Mitsui O.S.K. Lines.

NYK Line (TSE: 9101, -3.64%) has attempted decisive growth twice in recent weeks, but failed both times. Over the past two weeks, it has thus been sliding back toward the bases of these attempts. Before it drops to those levels, however, buyers will push the price slightly higher. The tug-of-war over future movement continues.

Capital Clean Energy Carriers (NASDAQ: CCEC, -3.37%) attempted to capitalise on the momentum following its return to the support zone. However, it failed, and the price closed below the previous close, though still within that support zone.

Excelerate Energy (NYSE: EE, -3.27%) is in a similar situation. It, too, attempted to rise from the support level, but unsuccessfully.

COSCO Shipping Energy Transportation (SS: 600026, -3.14%) tested the depth of support somewhat, but it held.

ADNOC Logistics & Services (ADX: ADNOCLS, -3.09%), on the other hand, has now fallen below the support level after a brief return to it. This is, of course, a reaction to the re-closure of the Strait of Hormuz and the continuing tensions, albeit during an extended ceasefire.

Mitsui O.S.K. Lines (TSE: 9104, -2.94%) also reached support. Here, too, a deeper decline was averted and mitigated.

There is only one stock left on the list of decliners: Nakilat (QSE: QGTS, -1.12%), which held its ground in the support zone and even slightly mitigated its decline during the week.

Among the gainers, Awilco LNG (OSE: ALNG) stood out the most, rising by five per cent. However, it continues to move sideways as investors gradually digest the company’s previous management announcements. Perhaps they’ll even come to like it.

Two growth companies also found favour in the top three. Exmar NV (EBR: EXM) gained 3.94%, and BP (NYSE: BP) rose 3.72%. We haven’t paid much attention to Exmar for some time, but nothing significant has happened, and the stock price continues to move sideways. BP, on the other hand, appears to be laying the groundwork for a new growth attempt, although from another perspective, it is still moving sideways below its peak.

Golar LNG and Shell posted nearly identical gains of 1.5%. Golar LNG (NASDAQ: GLNG) continues to hesitate regarding its next move. Shell halted the decline from the previous week.

However, the most popular number among rising companies wasn’t three; it was zero. That’s where the movement of three—or rather, four—companies begins.

Chevron (NYSE: CVX) slowed its decline with a 0.66% gain. Korea Line Corporation (KRX: 005880) consolidated its position with a 0.55% move; one could say it hammered in another lifeline for a new attempt to move higher. FLEX LNG (NYSE: FLNG) is trading in a narrow range above resistance. Attempts to rise are being rejected, but there is no downward pressure. The company is benefiting from spot rates, which are significantly higher than its long-term contracts for Atlantic routes.

Dynagas LNG (NYSE: DLNG) recorded zero weekly movement, but that does not mean nothing happened during the week. On the contrary, an attempt to rise within the sideways range, or a bounce off support, was unsuccessful. A move in the opposite direction was also rejected, though it was not as strong as the upward one.

Crystal Ball

The second quarter is typically the weakest seasonally, but this year will be different—geopolitical circumstances have knocked nearly 20% of global LNG production offline. While Europe still enjoys a certain advantage over Asia, it now needs gas, and rising prices are hitting the poorest consumers, such as those in Bangladesh, the hardest. Russia is trying to capitalise on the situation and offer an alternative, while Europe, paradoxically, is also increasing its imports of Russian LNG—partly in response to the U.S.’s unstable stance. On the other hand, unlike Russia, the United States remains a democracy.

The shortfall in supplies will have to be replaced. We view the return to coal as temporary; we expect a gradual increase in spot supplies and greater geographic diversification of sources, which will bring longer shipping routes and higher demand for tankers. Carriers operating on the US–Europe or Australia–Asia routes are in a more stable position.

The outlook remains volatile, but positive in the long term. Companies with spot tankers are benefiting from high rates and longer distances. The gradual phasing out of steamers and the addition of new liquefaction capacity will continue to drive the sector forward.

About UPI

Established in 2020, the UP World LNG Shipping Index is a rules-based family of stock indices designed to measure the performance of publicly traded companies worldwide engaged in the maritime transportation of liquefied natural gas (LNG). This unique index comprises 20 companies and partnerships worldwide, representing more than 65% of the global LNG carrier fleet in 2020. The UP Index provides premium services, offering freemium and trial access to charts. With the Freemium plan, users can access the basic UPI vs S&P 500 chart after completing email registration. The trial includes full access for fourteen days.

Final Note

This report primarily relies on technical analysis using weekly data. The summary section is AI-generated.