Summary

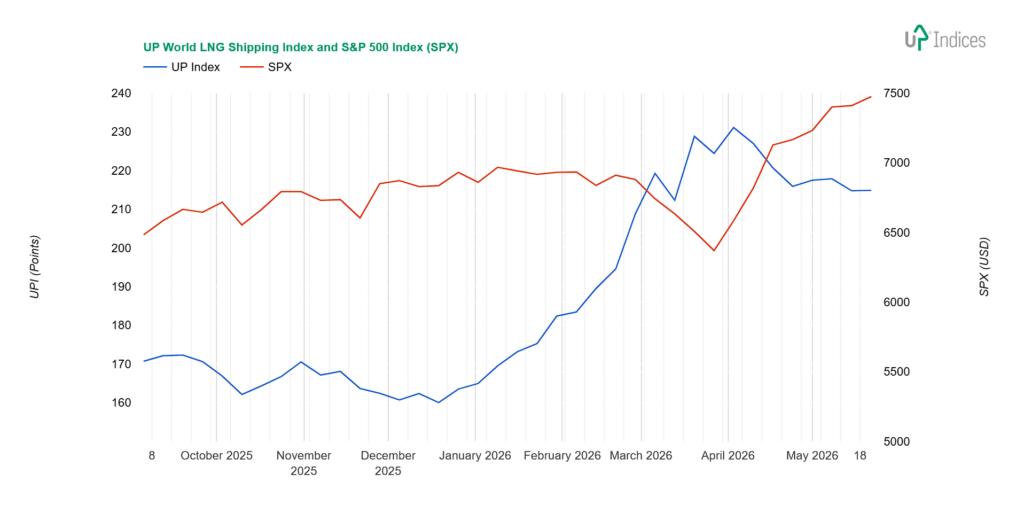

The UP World LNG Shipping Index gained 0.11 points (0.05%) last week, closing at 214.82 points, while the S&P 500 gained 0.88% — its eighth consecutive weekly gain, supported by optimism around Middle East peace negotiations. The UPI continues to move sideways within a support range roughly defined by 212 and 219 points. The median change was 0.14%; the weighted index fell by over 1%; and the ratio of advancing to declining stocks was 11:9. Trading volume remains at pre-war levels and continues to decline. Qatar has now smuggled a fifth tanker through the Strait of Hormuz with AIS turned off.

Exmar led the gainers with +7.37%, returning to last year’s price range, followed by Capital Clean Energy Carriers (+6.5%) and COSCO Shipping Energy Transportation (bouncing off support). On the downside, New Fortress Energy fell 8.78%, and Golar LNG dropped 8.2% — the latter following solid quarterly results that nevertheless failed to justify already priced-in optimism, compounded by silence on the strategic review. Mitsui O.S.K. Lines lost 3.63%, erasing the previous week’s gains. Both Gulf companies remained near their established levels. The long-term outlook stays positive.

UPI & SPX

The UP World LNG Shipping Index, which tracks 20 listed LNG shipping companies, gained 0.11 points (0.05%), closing at 214.82 points, while the S&P 500 index gained 0.88%. The chart below illustrates the performance of both indices with weekly data.

Broader View

The UPI continues to move sideways within a support range roughly defined by the 219- and 212-point levels. This is due to a geopolitical lull—or perhaps a stalemate—in which all parties not involved in the war are trying to resolve the problems that have arisen.

The median movement of the UPI was 0.14%; the weighted UPI index fell by over 1%; trading volume remains at pre-war levels and continues to decline. The ratio of advancing to declining stocks was 11:9.

Qatar has already smuggled a fifth tanker through the Strait of Hormuz with its Automatic Identification System (AIS) turned off; these five shipments together contain roughly 885,000 cubic meters of LNG, which corresponds to approximately 530 million cubic meters of natural gas, enough to supply electricity to a city of one million people for one year. So every shipment that gets through provides relief to the global market.

Asia remains the main consumer of LNG; Europe has until summer and appears to be hoping for a resolution to the situation. If that does not happen, natural gas prices will have to rise to redirect its flow.

Constituents

Exmar (EBR: EXM) recorded the largest gain, rising 7.37%. The price has thus returned to last year’s range.

Capital Clean Energy Carriers (NASDAQ: CCEC) moved higher within a broader sideways range, adding 6.5% to its price. Resistance for the stock is around $24 (closing price $22.31), so the main positive is that the downward price pressure seen in February appears to have been overcome.

COSCO Shipping Energy Transportation (SS: 600026) bounced off support again, settling near the peak of its New Year’s rally and now waiting for the fifth week.

Korea Line Corporation (KRX: 005880) posted the latest significant gain, up 3.61%. It, too, has settled in the support zone, waiting for further momentum.

Other positive moves were less than 1%: Excelerate Energy (NYSE: EE, +0.92%), Dynagas LNG Partners (NYSE: DLNG, +0.79%), Shell (NYSE: SHEL, +0.41%), and, for example, MISC (KLSE: 3816, +0.37%).

Excelerate Energy remains at its magnetic resistance level after breaking through the previous range; a true breakout would require a close above at least $37.72. Dynagas is at its support level and testing minor movements in both directions; Shell, like the other two oil companies, BP (NYSE: BP) and Chevron (NYSE: CVX), is primarily dependent on oil price movements. Over the past week, they traded in positive territory, but the closing price pulled them down. MISC has also been trading sideways since March.

Tsakos Energy Navigation (NYSE: TEN, -0.1%) attempted to rise, but its attempt to break through the short-term range at historical highs was rejected, suggesting buyers are running out of steam.

The biggest losses exceeded 8% and were suffered by New Fortress Energy (NASDAQ: NFE, -8.78%) and Golar LNG (NASDAQ: GLNG, -8.2%). NFE is trading sideways near its lows, while Golar fell following quarterly results that, while very good, were not enough to justify the already priced-in optimism. Furthermore, the silence regarding a potential sale or merger did not support the stock price.

Third in the list of declining stocks was Mitsui O.S.K. Lines (TSE: 9104), which lost 3.63%, erasing the previous week’s gains. The question of whether this marks a halt to the decline or merely a slowdown remains.

Another Japanese company, NYK Line (TSE: 9101), lost just under 2%. For this company, the decline appears to be continuing after a slowdown. In contrast, “K” Line (TSE: 9107, -0.5%) is moving sideways and consistently testing an upward move. It should be noted that these attempts have been unsuccessful.

Both Gulf companies lost only slightly. ADNOC Logistics & Services (ADX: ADNOCLS) lost 0.85%, and Nakilat (QSE: QGTS) lost 0.6%. Both are thus maintaining their previous levels—ADNOC at resistance, Nakilat at support.

FLEX LNG (NYSE: FLNG, -0.5%) continues to trade near this year’s highs; this week marks its ex-dividend date.

Awilco LNG (OSE: ALNG) is trading near support; it fell 0.3% last week.

Crystal Ball

The second quarter is typically the weakest seasonally, but this year will be different—geopolitical circumstances have knocked nearly 20% of global LNG production offline. While Europe still enjoys a certain advantage over Asia, it now needs gas, and rising prices are hitting the poorest consumers, such as those in Bangladesh, the hardest.

The shortfall in supplies will have to be replaced. We view the return to coal as temporary; we expect a gradual increase in spot supplies and greater geographic diversification of sources, which will bring longer shipping routes and higher demand for tankers.

Carriers operating on the US–Europe or Australia–Asia routes are in a more stable position.

The outlook remains volatile, but positive in the long term. Companies with spot tankers are benefiting from high rates and longer distances. The gradual phasing out of steamers and the addition of new liquefaction capacity will continue to drive the sector forward.

About UPI

Established in 2020, the UP World LNG Shipping Index is a rules-based family of stock indices designed to measure the performance of publicly traded companies worldwide engaged in the maritime transportation of liquefied natural gas (LNG). This unique index comprises 20 companies and partnerships worldwide, representing more than 65% of the global LNG carrier fleet in 2020. The UP Index provides premium services, offering freemium and trial access to charts. With the Freemium plan, users can access the basic UPI vs S&P 500 chart after completing email registration. The trial includes full access for fourteen days.

Final Note

This report primarily relies on technical analysis using weekly data. The summary section is AI-generated.