Summary

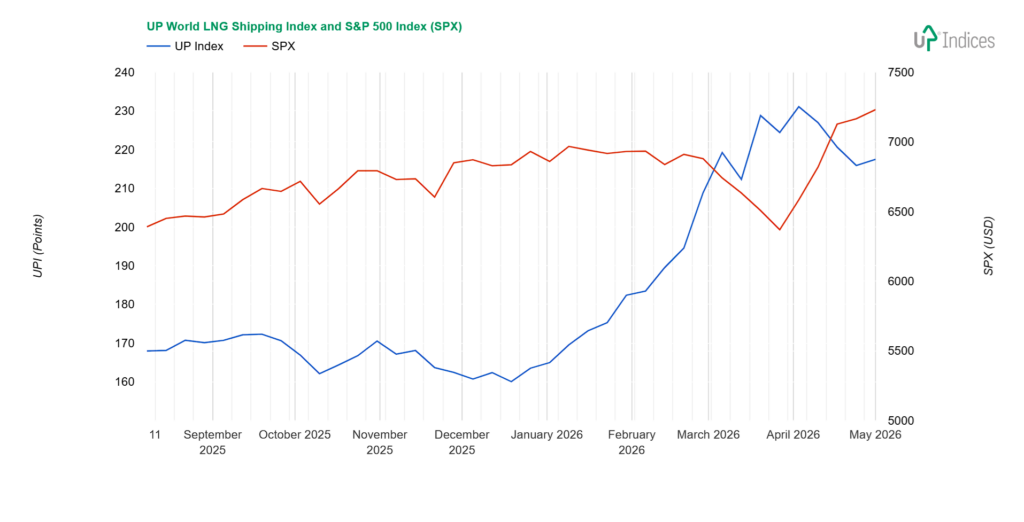

The UP World LNG Shipping Index gained 1.59 points (0.73%) last week, closing at 217.45 points, while the S&P 500 gained 0.91%. The headline number, however, tells only part of the story: the median gain was 2.37%, and gainers outnumbered decliners 13:7, yet the weighted index lost 4%. Three heavyweight constituents dragged the index down — Nakilat (20% weight, -2.73%), NYK Line (~7%, -4.17%), and Mitsui O.S.K. Lines (~9%, -3.35%) — while the majority of the index moved higher. The UPI chart remains constructive: after three weeks of decline, a slight recovery above this year’s low suggests the index is holding its ground above 210 points.

The Strait of Hormuz remains closed. Spot rates were little changed. Among the standout movers, ADNOC Logistics & Services surged 9.76%, returning to its highest levels since the turn of the year, driven by geopolitical calm rather than full resolution. Awilco LNG gained 9.95%, breaking away from its post-announcement decline and returning to October highs on increased volume — a shift in investor sentiment. Tsakos Energy Navigation rose nearly 8% to new highs. On the downside, Korea Line Corporation fell 6.15%, giving back part of its April gains. U.S. producers continue to make progress on new capacity: Golden Pass Train 2 is expected by the end of 2026, while Rio Grande LNG is on track for commissioning later this year and first LNG production in H1 2027.

UPI & SPX

The UP World LNG Shipping Index, which tracks 20 listed LNG shipping companies, gained 1.59 points (0.73%), closing at 217.45 points, while the S&P 500 index gained 0.91%. The chart below illustrates the performance of both indices with weekly data.

Broader View

The UPI rose slightly (up 0.73%), but an interesting comparison emerges when we factor in the median and weighted UPI. The median recorded the highest increase, 2.37%, but the weighted index lost 4%. When we also add the ratio of rising to falling stocks, which was 13:7 this time, it follows that most stocks rose, and larger stocks dragged down the weighted index. Specifically, Nakilat (20% weight, down 2.73%) and two Japanese companies: NYK Line (approx. 7% weight, down 4.17%) and Mitsui O.S.K. Lines (approx. 9% weight, down 3.35%).

For comparison: The three stocks with the highest growth posted double-digit gains (rounded), but their weightings were more or less well below 1%.

However, the UPI chart is also worth noting. After three weeks of decline, there was a slight recovery above this year’s low. Overall, the chart looks quite positive, which is why we wrote about the completion of the first phase of this year’s growth and the second quarter’s different trajectory. We therefore lean toward the UPI at least holding above 210 points.

The geopolitical situation remains unchanged. The Strait of Hormuz is closed, and a change could occur as early as this Monday, when the U.S. has announced it will escort ships through this narrow passage. It is hard to imagine this happening without Iran’s consent, as Iran is capable of—and likely willing to—deploy everything at its disposal against such a convoy. Defending against dozens of short-range targets is probably not something the U.S. Navy would want to face repeatedly.

Gas continues to flow mainly to Asia, with spot prices for LNG tankers easing slightly. U.S. producers are continuing to commission additional terminals: the second unit of the Golden Pass terminal is expected to be completed by the end of this year. Commissioning at the Rio Grande terminal is expected to be completed by the end of 2026, with first LNG production anticipated in H1 2027.

Constituents

New Fortress Energy (NASDAQ: NFE, +16.5%). We are used to big moves with this stock, and this time it is nothing significant either—the stock continues to trade sideways at support.

More interesting is the nearly 10% move in two other companies. Awilco LNG (OSE: ALNG, +9.95%) decided to test its strength, and the outcome was quite positive. The price broke away from its decline following the announcement of an expansion of operations and a new share offering, rising to October’s highs. An attempt at further gains, however, was rejected. But the very return to these levels—amid increased volume—signals a shift in investor sentiment.

The second-largest gainer was ADNOC Logistics & Services (ADX: ADNOCLS, +9.76%). With this sharp rise, it not only returned to pre-war levels but also reached the highest level seen at the turn of the year, though it remained slightly below that level. Optimism is driven by geopolitical calm, or rather, the lack of escalation of the current lull. However, the Strait of Hormuz remains closed.

Tsakos Energy Navigation (NYSE: TEN) posted a notable gain of nearly 8%, surging to new heights after a period of sideways consolidation. Volume, however, was below average.

Golar LNG (NASDAQ: GLNG) reached the resistance level of its top sideways trend with a 5.83% gain. The groundwork has thus been laid, and now a breakout attempt could follow.

FLEX LNG (NYSE: FLNG) is also making moves, gaining 4.3% and breaking out of its sideways range. The quarterly results announcement approaches and will be influenced by rising spot rates, while the dividend yield is falling below 9.5%. Nevertheless, the stock closed above previous highs.

Capital Clean Energy Carriers (NASDAQ: CCEC) gained 4%, though the price was significantly higher earlier in the week. Nevertheless, the stock continues to move sideways.

MISC (KLSE: 3816) posted a 3.33% gain and is pushing through increased volume in a sideways range toward resistance.

Chevron (NYSE: CVX, +2.9%) bounced off support, but the next direction is still undecided—it could be an attempt to resume growth, in which case it would need to break above $215, or a correction of the decline. In that case, the behaviour around $185 will be decisive.

Excelerate Energy (NYSE: EE) continues to move sideways despite a 2.1% gain, while COSCO Shipping Energy Transportation (SS: 600026) confirmed its support level, rebounded from it, and rose 1.6%.

The biggest loser was Korea Line Corporation (KRX: 005880), which fell 6.15% and dropped below the lows of the previous weeks. However, the positive effect of the 30% rise from early April still prevails.

We have already mentioned the other declining companies. Both Japanese companies reached their support levels, and Nakilat fell back below its support. However, it is holding steady there for now. “K” Line (TSE: 9107) also reached its support level, losing 1.59%.

Crystal Ball

The second quarter is typically the weakest seasonally, but this year will be different—geopolitical circumstances have knocked nearly 20% of global LNG production offline. While Europe still enjoys a certain advantage over Asia, it now needs gas, and rising prices are hitting the poorest consumers, such as those in Bangladesh, the hardest. Russia is trying to capitalise on the situation and offer an alternative, while Europe, paradoxically, is also increasing its imports of Russian LNG—partly in response to the U.S.’s unstable stance. On the other hand, unlike Russia, the United States remains a democracy.

The shortfall in supplies will have to be replaced. We view the return to coal as temporary; we expect a gradual increase in spot supplies and greater geographic diversification of sources, which will bring longer shipping routes and higher demand for tankers. Carriers operating on the US–Europe or Australia–Asia routes are in a more stable position.

The outlook remains volatile, but positive in the long term. Companies with spot tankers are benefiting from high rates and longer distances. The gradual phasing out of steamers and the addition of new liquefaction capacity will continue to drive the sector forward.

About UPI

Established in 2020, the UP World LNG Shipping Index is a rules-based family of stock indices designed to measure the performance of publicly traded companies worldwide engaged in the maritime transportation of liquefied natural gas (LNG). This unique index comprises 20 companies and partnerships worldwide, representing more than 65% of the global LNG carrier fleet in 2020. The UP Index provides premium services, offering freemium and trial access to charts. With the Freemium plan, users can access the basic UPI vs S&P 500 chart after completing email registration. The trial includes full access for fourteen days.

Final Note

This report primarily relies on technical analysis using weekly data. The summary section is AI-generated.